Critics warn health-care loans could deepen financial burdens for low-income families

A proposal by the Trump administration to allow health insurers to offer loans to Affordable Care Act (ACA) enrollees struggling with medical bills has sparked growing controversy among health policy experts, consumer advocates, and state officials.

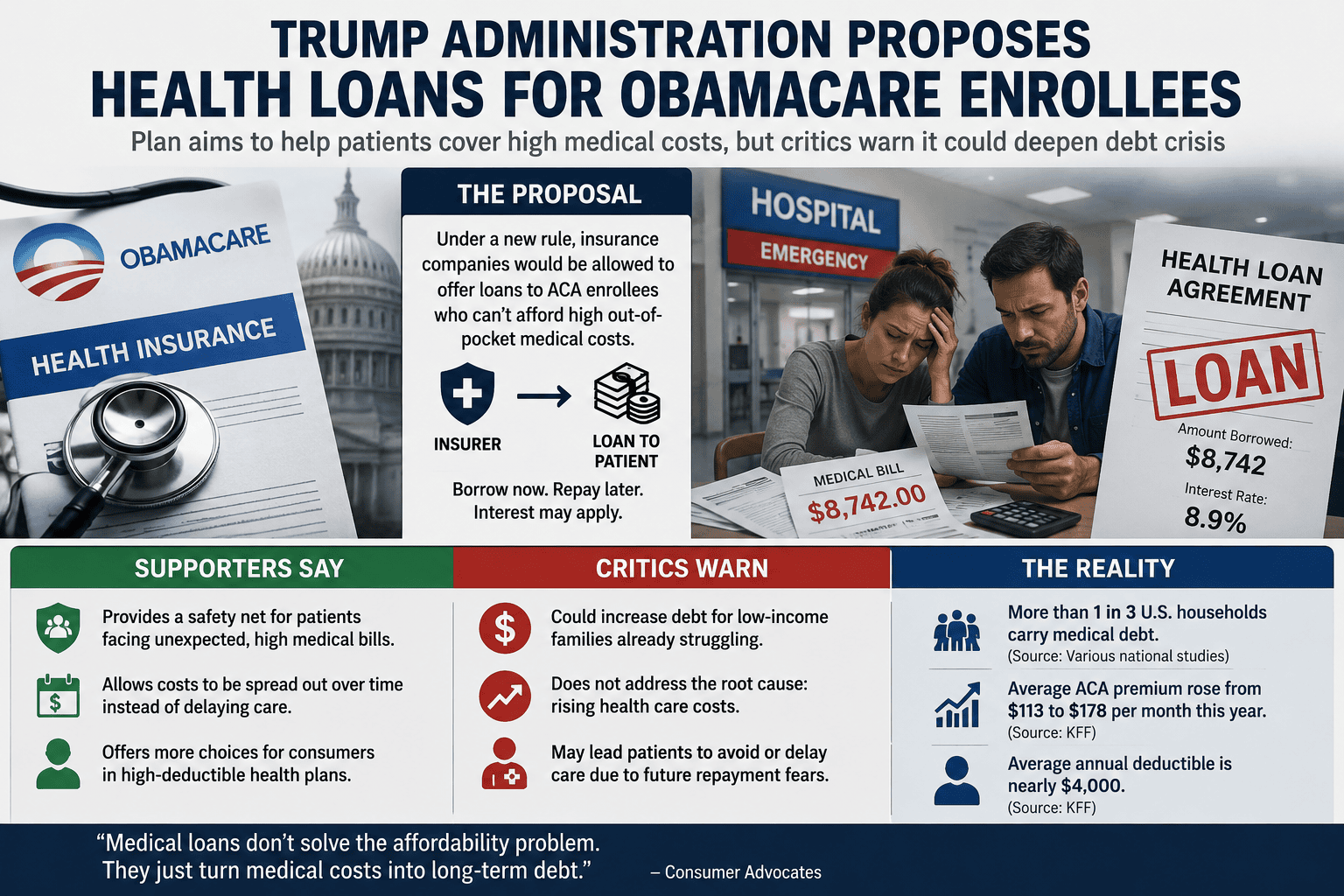

According to a recent report by The New York Times, the administration included the idea in a sweeping final rule governing ACA marketplace plans released last month. The proposal would permit insurance companies to provide financing options to policyholders who are unable to pay large out-of-pocket medical expenses resulting from serious illnesses, emergency treatment, or hospitalization.

Under the proposal, patients facing high deductibles or other cost-sharing obligations could borrow money from their insurance provider and repay the amount over time, potentially with interest.

Administration officials argue that the measure would provide a safety net for consumers enrolled in lower-premium, high-deductible health plans. Supporters say the financing option could help families avoid delaying treatment when unexpected medical expenses arise.

However, critics contend that the proposal addresses the symptom rather than the root cause of rising health-care costs.

Consumer advocacy groups and medical experts argue that encouraging patients to borrow money for health care could worsen an already serious medical debt crisis. More than one-third of U.S. households currently carry some form of medical debt, according to various national studies.

“This does not reduce medical costs; it simply changes how those costs are paid,” critics argue.

Stanford University economist Neale Mahoney criticized the concept, saying that increasing deductibles while encouraging people to take on additional debt is disconnected from the financial realities many families face.

The debate comes as ACA enrollees continue to experience rising costs. Following the expiration of enhanced federal premium subsidies approved during the pandemic, many consumers have seen significant increases in monthly insurance premiums.

According to data from the Kaiser Family Foundation (KFF), average monthly ACA premiums increased from approximately $113 last year to $178 this year. Average annual deductibles are approaching $4,000, while some Bronze-level plans carry maximum out-of-pocket costs exceeding $10,000 for an individual.

The administration is also pursuing broader reforms aimed at expanding access to lower-cost, higher-deductible insurance products. Beginning in 2027, eligibility for catastrophic health plans is expected to expand. By 2028, some family plans could carry deductibles exceeding $31,000.

Supporters of the reforms argue that higher-deductible plans encourage consumers to become more price-conscious when seeking medical care and may help reduce unnecessary spending within the health-care system.

Opponents counter that such plans often discourage patients from seeking preventive care or necessary treatment because of cost concerns. Research from Johns Hopkins University has found that individuals carrying medical debt are significantly more likely to delay or forgo medical, dental, and mental health services.

Even within the insurance industry, enthusiasm for the proposal appears limited. Health policy analyst Louise Norris said it remains unclear whether insurers or consumers will embrace medical lending programs.

“Borrowing money may provide short-term relief,” Norris noted, “but it could ultimately create greater financial pressure for families already struggling to make ends meet.”

Several state governments and consumer groups have already filed legal challenges against the broader ACA rule changes. Opponents claim the new regulations could make coverage less affordable, increase out-of-pocket costs, and potentially leave millions of Americans uninsured.

At the center of the debate is a fundamental question: Should health-care affordability be addressed by expanding access to credit, or by lowering the cost of medical care itself?

For critics, the answer is clear. They argue that medical loans do not solve the underlying affordability problem. Instead, they risk transforming health-care expenses into long-term debt obligations for the very families the ACA was designed to protect.

{kind=link}