The U.S. economy added only 57,000 nonfarm payroll jobs in June, far below expectations of roughly 110,000. The unemployment rate slipped from 4.3% to 4.2%, but the decline was not as reassuring as it looked. The labor force participation rate fell to 61.5%, and the number of people in the labor force dropped. In other words, the jobless rate improved partly because fewer people were counted as looking for work.

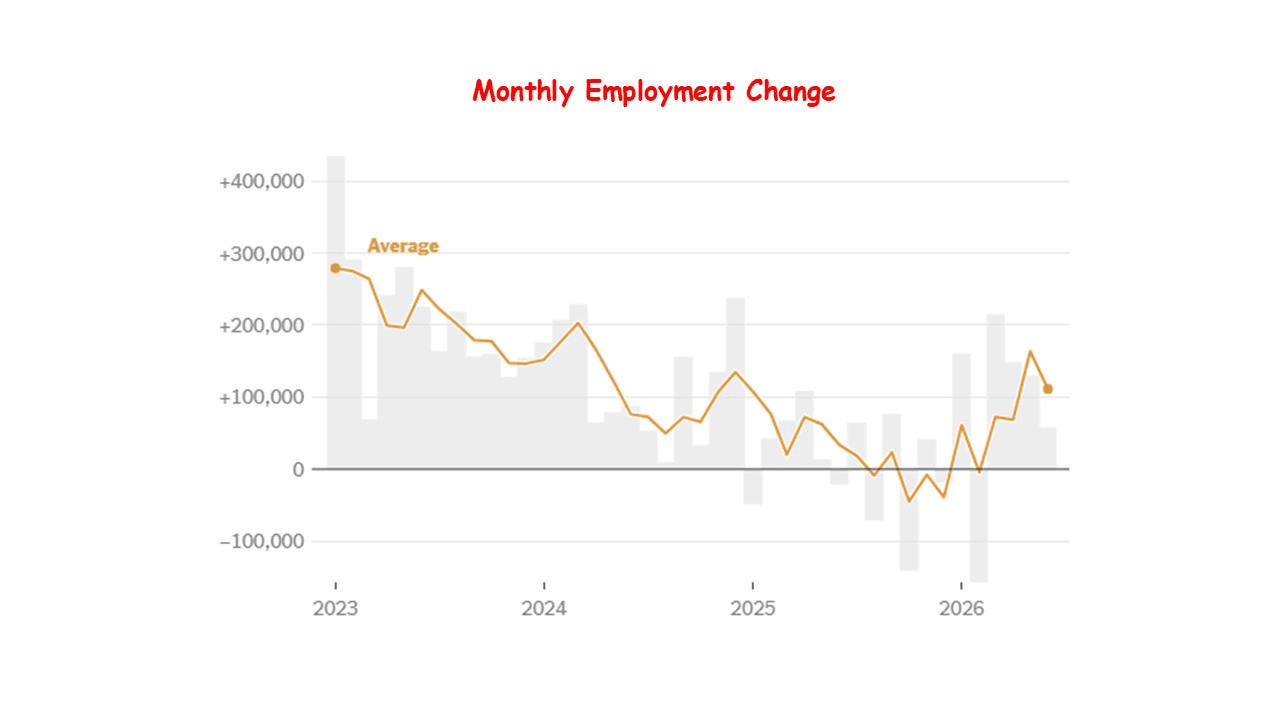

The bigger story is that the labor market’s softening trend is becoming harder to dismiss. A single weak month can be noise. But June came with a large downward revision to the prior two months: April and May employment were 74,000 lower than previously reported. After revisions, job gains averaged about 111,000 per month over the past three months, respectable but clearly slower than the May report had suggested. More striking, BLS said payroll growth averaged only 36,000 per month over the prior 12 months. It is no longer a hot labor market. It is a labor market running on a thinner cushion.

The bigger story is that the labor market’s softening trend is becoming harder to dismiss. A single weak month can be noise. But June came with a large downward revision to the prior two months: April and May employment were 74,000 lower than previously reported. After revisions, job gains averaged about 111,000 per month over the past three months, respectable but clearly slower than the May report had suggested. More striking, BLS said payroll growth averaged only 36,000 per month over the prior 12 months. It is no longer a hot labor market. It is a labor market running on a thinner cushion.

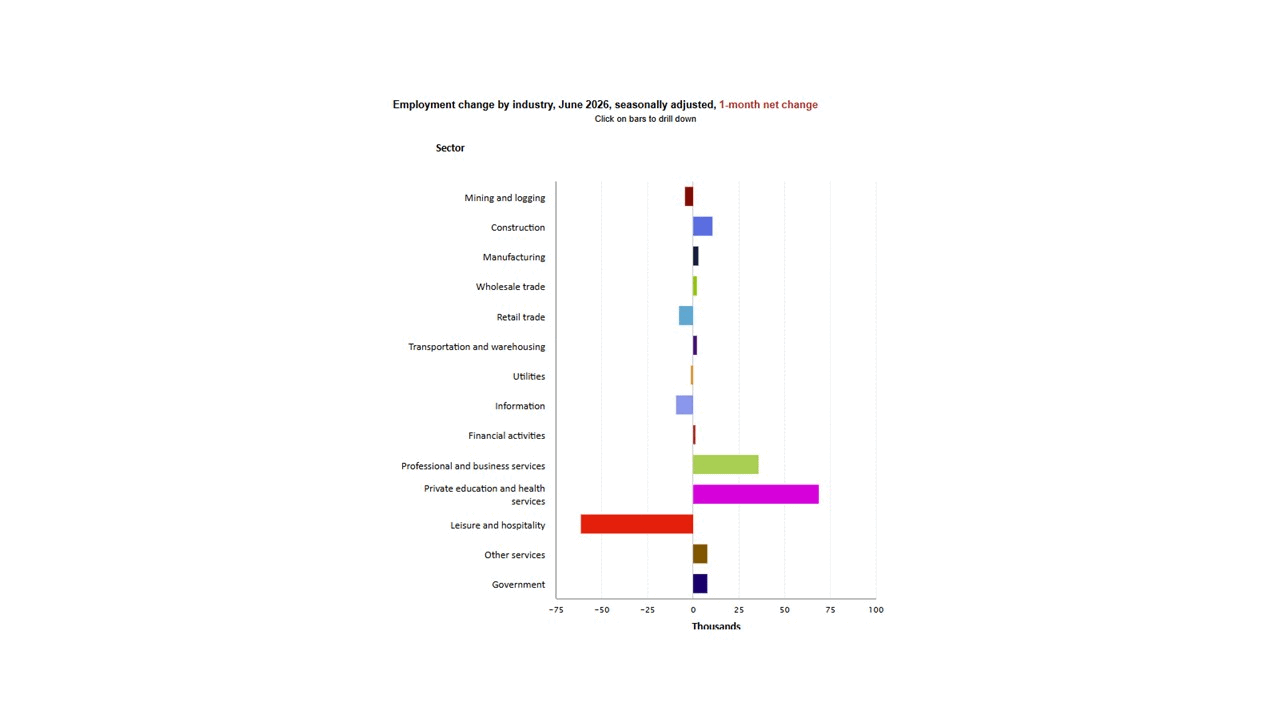

The composition of hiring also remains narrow. Health care and social assistance are still doing much of the heavy lifting. In June, healthcare added about 22,000 jobs, while social assistance added about 25,000, for a combined gain of roughly 47,000 jobs. That was more than 80% of the total payroll gain. Health care hiring itself slowed: the June increase of 22,000 was well below its average monthly gain of 38,000 over the prior year. Social assistance remained firm, led by individual and family services.

Leisure and hospitality were the weakest spot. Employment in the sector fell by 61,000 in June, with accommodation and food services accounting for most of the decline. BLS described this as “weaker than usual seasonal hiring,” not simply normal seasonality. That distinction matters. June is usually a strong month for travel, restaurants, hotels, and entertainment. A seasonally adjusted decline means hiring was weaker than expected for this time of year. Some of this may be payback after earlier strength, but it also raises a broader concern: lower-income consumers may be pulling back, and service employers may be less confident about summer demand.

The household survey added another note of caution. The labor force participation rate fell 0.3 percentage point, employment declined, and the number of people not in the labor force increased. The labor force can shrink for several reasons: retirements, weaker job-search confidence, reduced immigration flows, family-care constraints, and simple month-to-month volatility. Recent reporting has also emphasized that slower immigration has lowered the “break-even” pace of job growth needed to keep unemployment stable. That helps explain why the unemployment rate can remain low even when payroll growth slows. A smaller labor-supply pipeline can make the labor market look tighter than it really feels to job seekers.

The household survey added another note of caution. The labor force participation rate fell 0.3 percentage point, employment declined, and the number of people not in the labor force increased. The labor force can shrink for several reasons: retirements, weaker job-search confidence, reduced immigration flows, family-care constraints, and simple month-to-month volatility. Recent reporting has also emphasized that slower immigration has lowered the “break-even” pace of job growth needed to keep unemployment stable. That helps explain why the unemployment rate can remain low even when payroll growth slows. A smaller labor-supply pipeline can make the labor market look tighter than it really feels to job seekers.

For the Federal Reserve, the report reduces the case for another rate hike, but it does not automatically open the door to rate cuts. Wage growth was still moderate, with average hourly earnings up 0.3% in June and 3.5% from a year earlier. That is not an overheating wage number. Markets read the report as less hawkish: the dollar weakened after the jobs data, and market odds of a Fed rate hike by September fell from 67% to 49%. Still, the Fed will remain cautious because inflation risk has not disappeared. A soft payroll number gives the Fed more breathing room, not a green light to declare victory.

Bottom line: the June report changes the labor-market story. The economy is not shedding jobs in a recessionary way, but the hiring engine is sputtering. Payroll growth is slower, revisions are negative, labor-force participation has fallen, leisure and hospitality is weakening, and job gains remain heavily dependent on health care and social assistance. This is no longer a booming labor market. It is a “low-hire, low-fire” economy with less margin for error. The Fed is now less likely to hike soon, the dollar has weakened on that expectation, and investors will increasingly ask if the cooling trend will continue.

Sung Won Sohn,PhD

Professor of Finance and Economics, Loyola Marymount University

Chief economist SSeconomics

{kind=link}