Critics say proposal would effectively cut benefits

Critics say proposal would effectively cut benefits

New projections offer slight relief but reform pressure remains

A growing debate is emerging in Washington over proposals to raise the Social Security full retirement age as lawmakers search for ways to address the program’s long-term funding challenges.

Critics argue that increasing the retirement age would amount to a significant benefit cut for millions of future retirees, particularly lower-income Americans who depend heavily on Social Security as a primary source of retirement income.

Sen. Elizabeth Warren (D-Mass.) recently joined fellow Democratic senators Tammy Duckworth and Richard Blumenthal in criticizing proposals supported by some Republicans to address the program’s projected funding shortfall.

“Republicans have a history of attempting to raise the retirement age, privatize Social Security, or otherwise cut benefits,” Warren wrote in a letter addressing the issue. She argued that proposals to increase the retirement age or impose means testing would effectively reduce benefits for retirees.

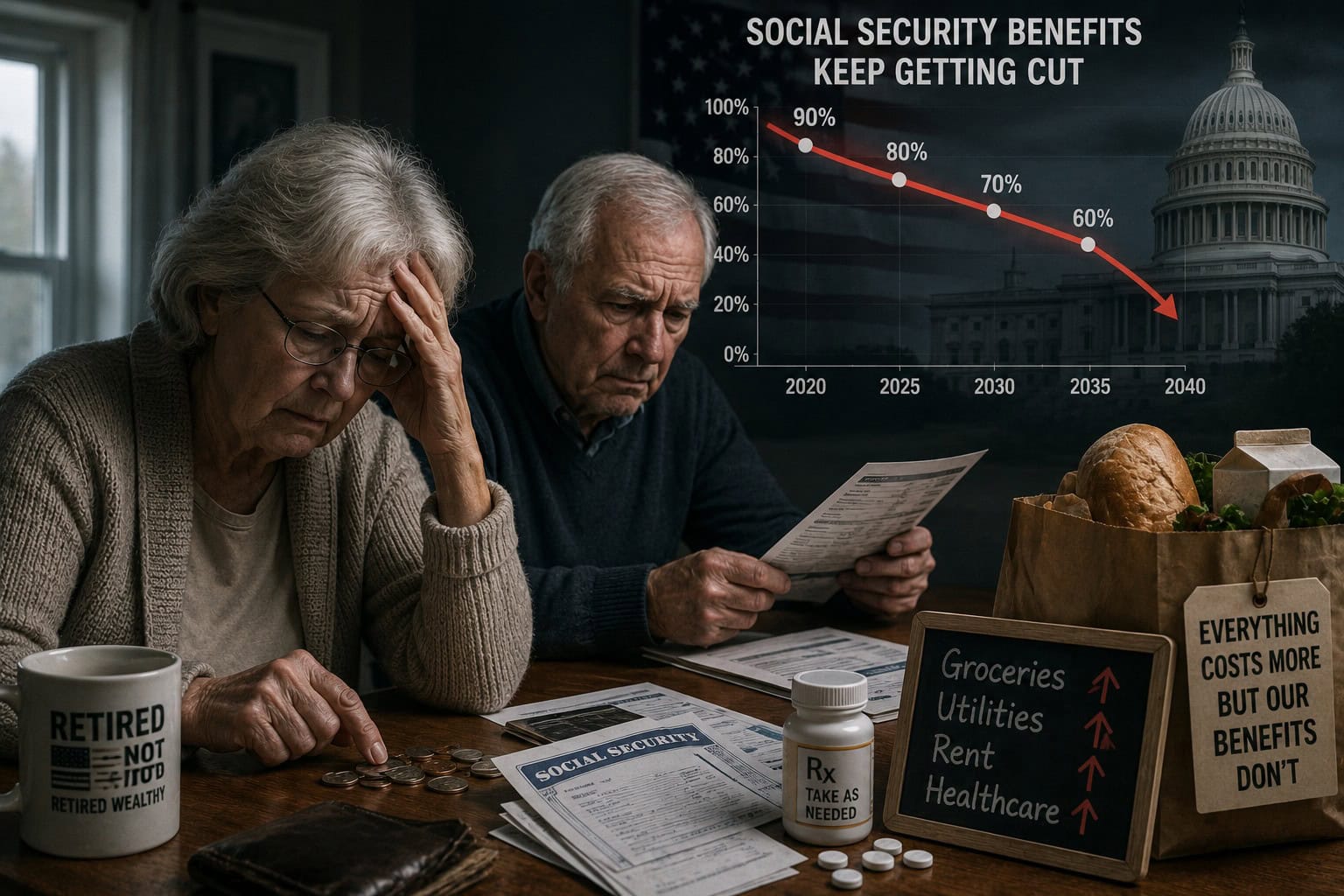

Warren specifically highlighted estimates showing that raising the full retirement age by two years could reduce monthly benefits for a typical retiree by between $345 and $741 per month. That would represent a reduction of roughly 17% to 35%, depending on when benefits are claimed.

“This would effectively cut Social Security benefits for tens of millions of Americans,” Warren said, noting that lower-income seniors would likely be affected the most.

According to Warren, the reduction would be similar in magnitude to the automatic benefit cuts that could occur if Social Security’s trust funds become insolvent and are only able to pay a portion of scheduled benefits.

The debate comes as concerns grow over the financial future of the nation’s largest retirement program.

A recent long-term analysis from the Penn Wharton Budget Model (PWBM) projects that Social Security’s Old-Age and Survivors Insurance (OASI) trust fund will be depleted in February 2033. While that estimate is slightly more optimistic than the Social Security trustees’ forecast of depletion during the fourth quarter of 2032, it still highlights the urgency of reform.

When disability insurance reserves are included, PWBM projects that the combined trust funds could remain solvent until February 2035, compared with the Social Security trustees’ estimate of depletion in the third quarter of 2034.

Importantly, depletion does not mean Social Security would go bankrupt. Payroll taxes paid by workers and employers would continue to fund benefits. However, without legislative action, incoming revenue would not be sufficient to cover all promised payments.

PWBM estimates that approximately 86% of scheduled benefits could still be paid immediately after trust fund depletion. Over the longer term, that percentage could decline to about 60% by the end of the century.

The report underscores the difficult choices facing lawmakers.

Kent Smetters, faculty director of the Penn Wharton Budget Model, warned that delaying reform will only increase the size of the adjustments eventually required.

“We’re still talking about a pretty sizable increase in taxes or reduction in benefits going forward,” Smetters said. “If we don’t act soon, the necessary changes will only become larger.”

PWBM estimates Social Security’s long-term actuarial deficit at 4.65% of taxable payroll, slightly higher than the Social Security trustees’ estimate of 4.42%.

To eliminate the shortfall solely through taxes, the current combined payroll tax rate of 12.4% would need to rise to approximately 17.1%, according to the analysis. That would increase contributions from both employees and employers and likely face strong political resistance.

As Congress weighs its options, proposals ranging from raising payroll taxes and lifting income caps to reducing future benefits and increasing the retirement age remain on the table.

While the projected depletion date may have moved back by a few months, experts agree that the underlying challenge remains unchanged: without reform, Americans will eventually face some combination of higher taxes, lower benefits, or longer working lives.

By Inseong Choi

{kind=link}