Rising property taxes, insurance premiums, and utility bills strain seniors’ budgets

As soaring home prices make homeownership increasingly difficult for younger Americans, many retirees are discovering that owning a home does not necessarily guarantee financial security.

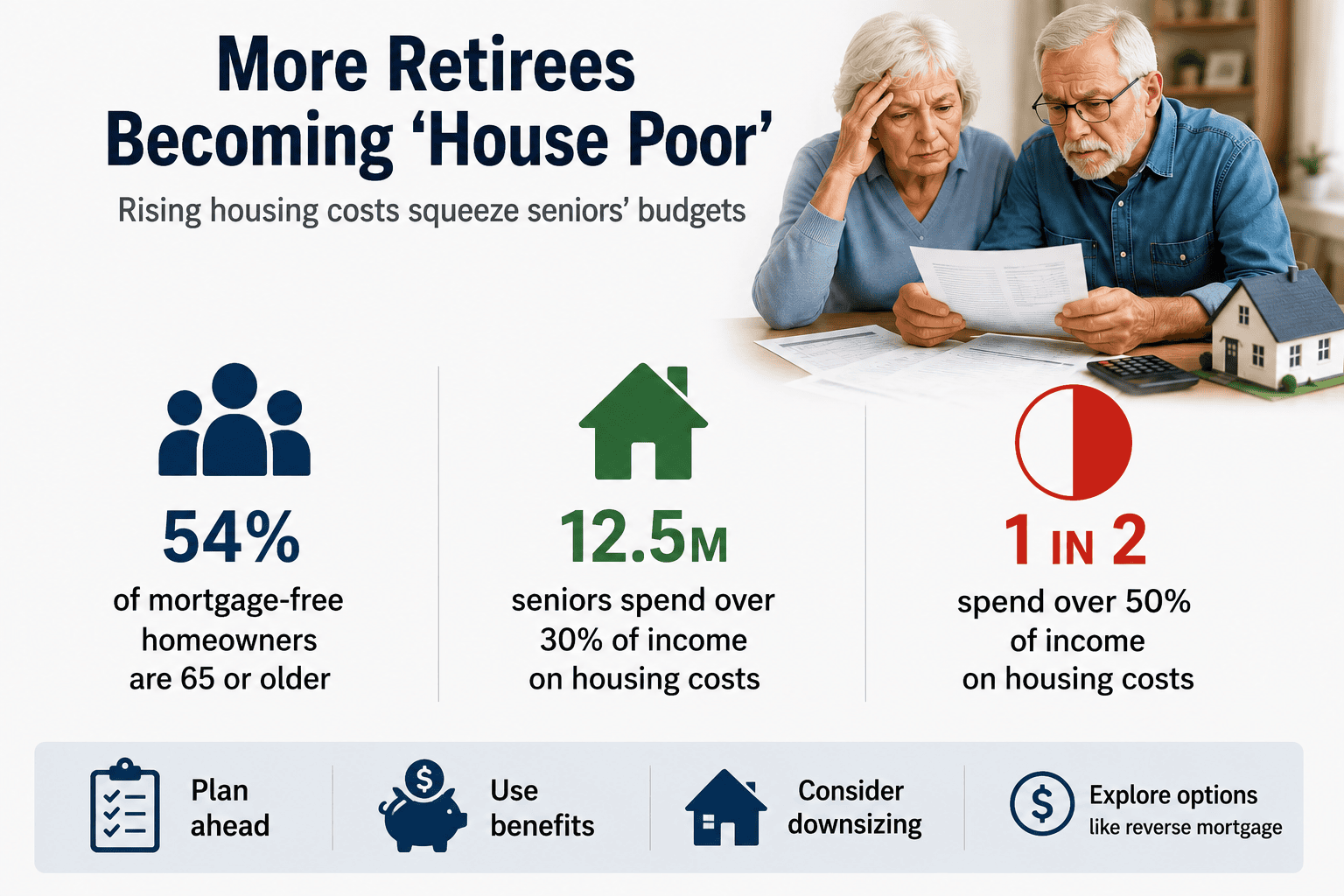

A growing number of older homeowners are becoming “house poor” — spending a large portion of their income on housing-related expenses despite having paid off their mortgages.

According to housing data recently cited by USA TODAY, approximately 35 million homeowners in the United States own their homes free and clear of a mortgage. More than half of them — about 54% — are age 65 or older. While nearly two-thirds of senior homeowners have fully paid off their homes, many continue to struggle with rising housing costs.

In 2024, an estimated 12.5 million senior households spent more than 30% of their income on housing expenses, placing them in the category of “cost-burdened” homeowners. Roughly half of those households spent more than 50% of their income on housing-related costs.

Housing experts generally consider a household financially burdened when housing expenses exceed 30% of total income. Those costs include mortgage payments, rent, property taxes, homeowners insurance, utilities, and maintenance expenses.

The trend highlights a growing reality for retirees: paying off a mortgage does not eliminate the financial obligations of homeownership.

Since the COVID-19 pandemic, many housing-related costs have risen sharply. National rents have increased by roughly 36%, while property taxes have climbed about 30% compared with 2019 levels. Homeowners insurance premiums have risen by more than 40%, and electricity costs have increased by nearly 40% since 2020.

For retirees living on fixed incomes, those increases can create significant financial stress.

“Even seniors who own their homes outright are not immune to rising housing costs,” said Christine Healy, brand leader at long-term care services company CareScout. “Property taxes, insurance premiums, maintenance expenses, and utility bills can quickly consume retirement savings, particularly for households relying on Social Security and fixed retirement income.”

Regional differences also play a major role.

California ranks among the states with the highest housing-related expenses for retirees, driven by elevated home values, rising insurance costs, and increasing utility rates. In contrast, states such as West Virginia offer significantly lower property taxes and insurance costs, making them more affordable for retirees on fixed incomes.

The growing burden has prompted financial planners to urge Americans to think beyond simply paying off a mortgage when preparing for retirement.

Experts recommend developing long-term financial plans that account for ongoing housing expenses, including taxes, insurance, maintenance, and utilities. They also encourage retirees to take advantage of available property tax relief programs and senior assistance benefits offered by local and state governments.

For some homeowners, downsizing to a smaller property may provide meaningful financial relief. Others may consider a reverse mortgage to access home equity while remaining in their homes, although financial advisors caution that such decisions should be carefully evaluated because of fees, repayment terms, and estate-planning considerations.

For decades, homeownership has been viewed as a cornerstone of retirement security and the American dream. However, rising housing costs are forcing many retirees to rethink that assumption.

As property taxes, insurance premiums, and utility costs continue to increase, owning a home may no longer guarantee financial comfort in retirement. Instead, for a growing number of seniors, the family home is becoming both a valuable asset and a significant financial burden.

{kind=link}