The labor market was supposed to limp. Instead, it jogged. It was supposed to whisper “slowdown.” Instead, it shouted, “Not so fast.” The May jobs report was not a fireworks show, but it was a lot stronger than the gloomy expectations many had at the end of 2025.

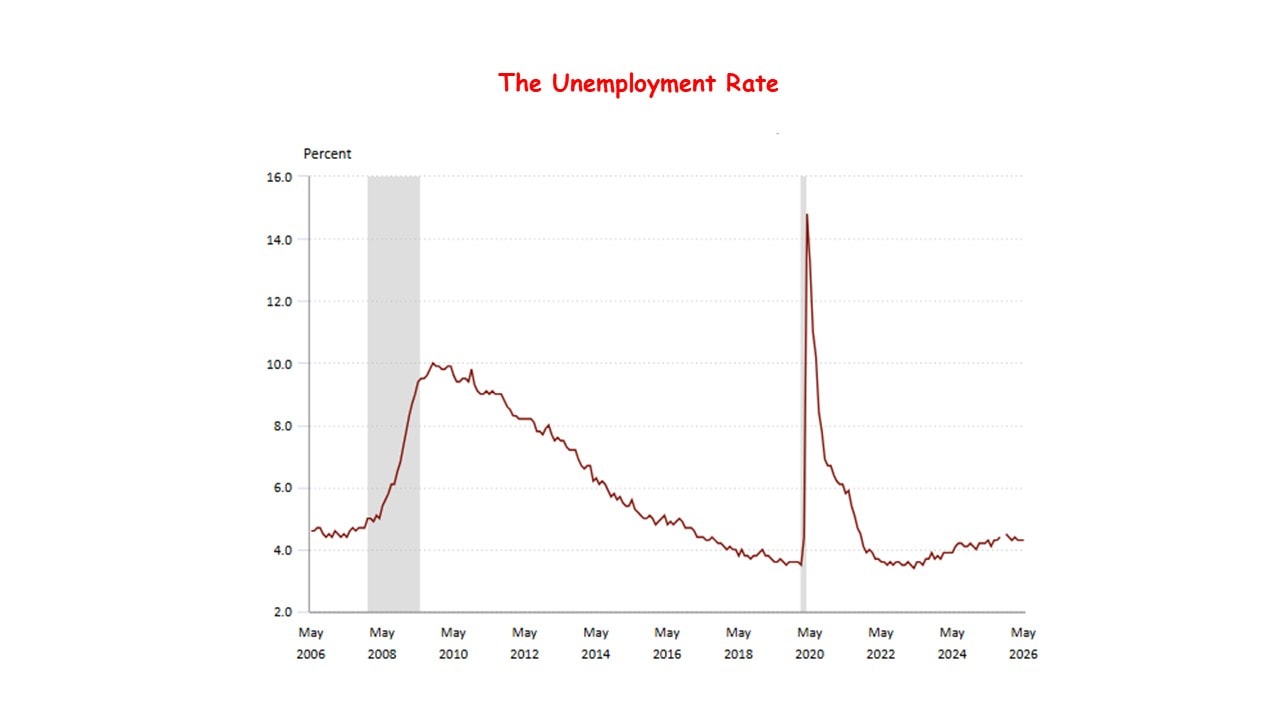

The U.S. economy added 172,000 jobs in May, while the unemployment rate held steady at 4.3%. That is a solid report by almost any reasonable standard. It shows that the economy is slowing from the red-hot post-pandemic pace, but it is not cracking. Consumers are still spending, businesses are still hiring, and the job market remains one of the strongest pillars holding up the economy.

Even more important, the previous two months looked better after revisions. March payrolls were revised up by 29,000, from 185,000 to 214,000. April was revised up by 64,000, from 115,000 to 179,000. Together, March and April were 93,000 jobs stronger than first reported. That matters. Revisions can change the story, and this time they made the labor market look healthier, not weaker.

Even more important, the previous two months looked better after revisions. March payrolls were revised up by 29,000, from 185,000 to 214,000. April was revised up by 64,000, from 115,000 to 179,000. Together, March and April were 93,000 jobs stronger than first reported. That matters. Revisions can change the story, and this time they made the labor market look healthier, not weaker.

Over the past three months, job gains averaged 188,000 per month. That is much better than what many economists and investors expected at the end of 2025, when fears of a sharper slowdown were widespread. Instead of falling into a ditch, the labor market has stayed on the road.

Without the war in the Middle East, the job gains probably would have been even stronger. The war has added uncertainty, raised energy concerns and made some businesses more cautious. Higher oil prices and geopolitical anxiety act like a tax on confidence. Companies may still hire, but they hesitate before expanding aggressively. Consumers may still spend, but they become more careful. In that sense, the May jobs report is impressive because it came despite a difficult global backdrop.

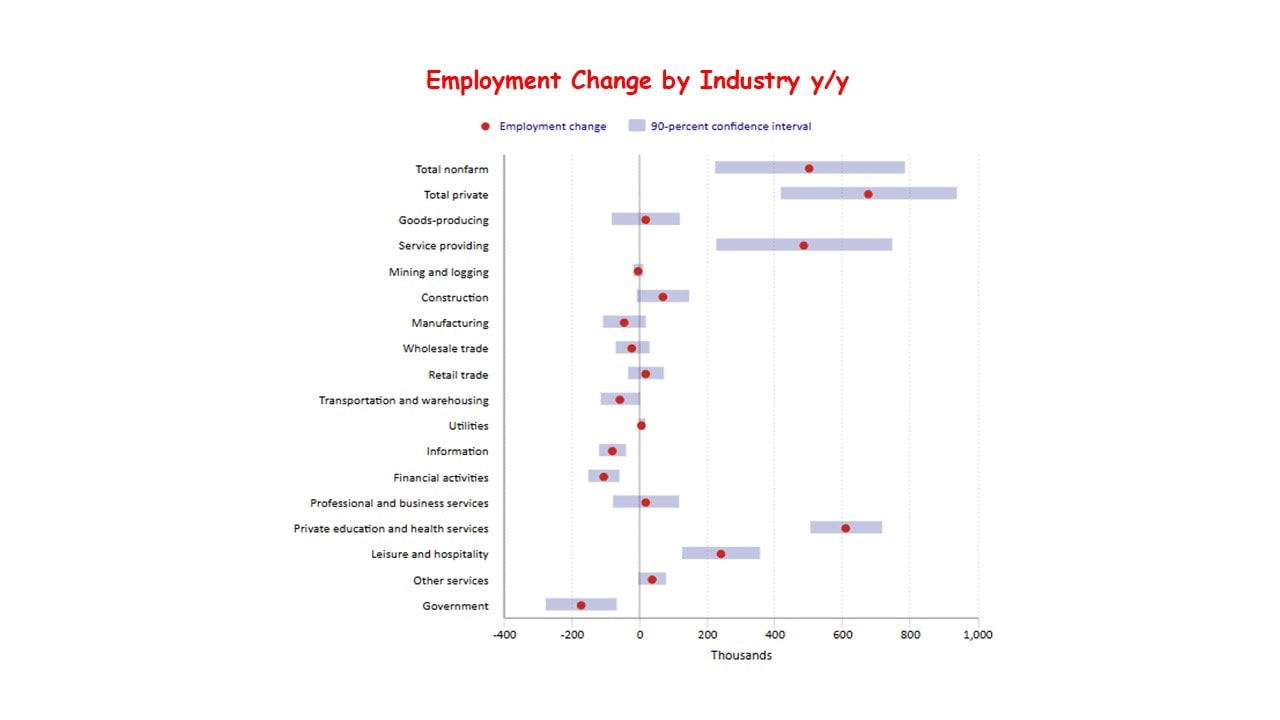

The gains were also fairly broad. Leisure and hospitality added 70,000 jobs, far above its recent average. Food services and drinking places were especially strong. Health care added 35,000 jobs, continuing its steady role as a dependable source of employment. Local government added 55,000 jobs. Social assistance continued to grow. Mining and energy-related employment also improved. Manufacturing was not booming, but it did not collapse either, and factory hours remained stable. The key point is that job creation was not limited to one tiny corner of the economy.

There were weak spots. Financial activities lost 22,000 jobs in May and are down sharply from a year earlier. Transportation and warehousing were essentially flat and remain below their earlier peak. Professional and business services, construction, retail and information showed little change. This tells us the economy is not racing ahead. It is moving forward, but with some sectors carrying more of the load than others.

There were weak spots. Financial activities lost 22,000 jobs in May and are down sharply from a year earlier. Transportation and warehousing were essentially flat and remain below their earlier peak. Professional and business services, construction, retail and information showed little change. This tells us the economy is not racing ahead. It is moving forward, but with some sectors carrying more of the load than others.

Wages also deserve attention. Average hourly earnings rose 0.3% in May and were up 3.4% from a year earlier. That is good news for workers, but it is not entirely comforting for the Federal Reserve. Wage growth has cooled from earlier highs, but it is still strong enough to keep inflation concerns alive, especially in services.

That is why this report complicates the Fed’s job. A weak labor market would have given the Fed room to focus on supporting growth. This report does the opposite. It tells the Fed that the job market is still solid enough for policymakers to keep their eyes on inflation. Rate cuts are now harder to justify. If inflation remains stubborn or energy prices rise further because of the Middle East war, the possibility of higher interest rates cannot be ruled out.

For financial markets, this is a mixed message. Strong job growth supports consumer spending and corporate earnings. But it also means the Fed may stay tough for longer. Good economic news can become bad market news if it pushes interest rates higher.

The bottom line is simple: the labor market is bending, but it is not breaking. Hiring remains solid, unemployment is stable, and revisions made the recent past look better. The economy still has momentum. The Fed may welcome the strength, but it will not celebrate too loudly. With inflation still the main enemy, a strong job market gives the Fed less reason to blink.

Sung Won Sohn,PhD

Professor of Finance and Economics, Loyola Marymount University

Chief economist SSeconomics

{kind=link}